MSME Loan vs Business Loan vs Working Capital Key Differences, Benefits & Which Is Best for Your Business

If you’re a business owner or established entrepreneur, understanding the right financing option can be the difference between growth and stagnation. In today’s competitive market, MSME business loans, business loans, and working capital loan options serve different cash needs and strategic purposes for the company of all sizes.

The key differences between MSME loans, business loans, and working capital loans explore their benefits to help you decide which type of loan is the best fit for your business needs.

Understanding the Basics

1. MSME Loan

An MSME loan is specifically designed for micro, small, and medium enterprises (MSMEs). It often comes with government support, easier eligibility, and flexible terms tailored to small and medium businesses. These loans aim to boost MSME funding for operational needs, inventory purchases, technology upgrades and more.

2. Business Loan

A business loan is a broader category of financing that isn’t limited to MSMEs. This loan is used for general purposes including business expansion financing, asset purchases, technology implementation and long term growth strategies.

3. Working Capital Loan

A working capital loan is short term financing meant to manage cash flows and cover daily expenses such as payroll, rent, utilities, supplier payments, or funds for operational expenses. It’s focused on helping businesses maintain liquidity rather than funding growth projects.

| Criteria | Micro Enterprise | Small Enterprise | Medium Enterprise | Large Enterprise |

|---|---|---|---|---|

| Annual Turnover | Up to ₹5 crore | Up to ₹50 crore | Up to ₹250 crore | Above ₹250 crore |

| Business Structure | Proprietorship, Partnership | Proprietorship, LLP, Pvt Ltd | LLP, Pvt Ltd | Pvt Ltd / Public Ltd |

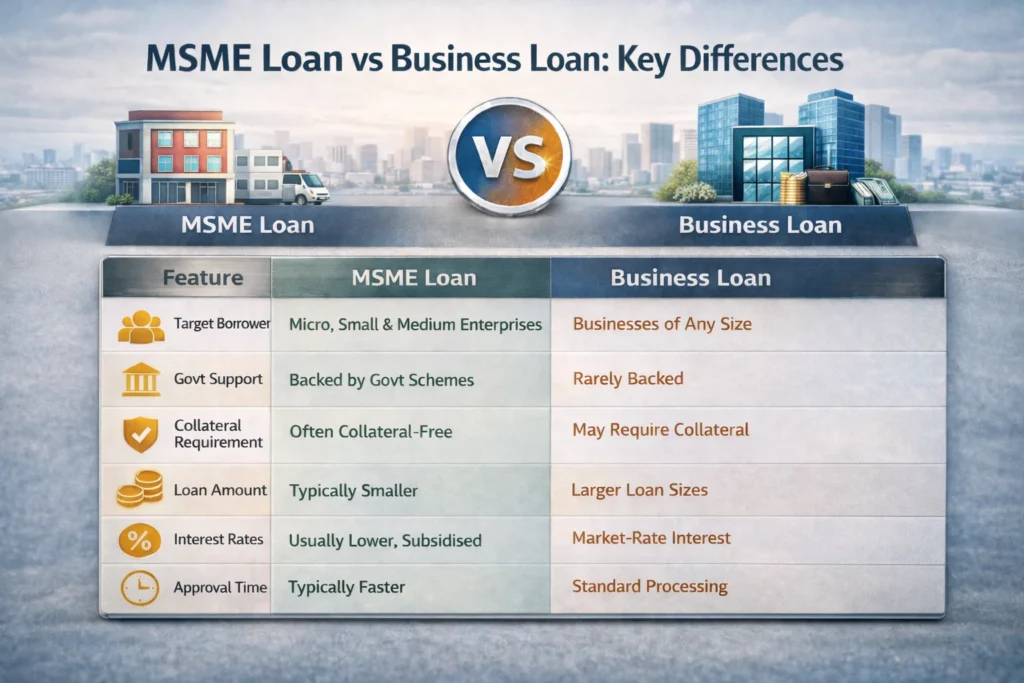

MSME Loans & Business Loans

Here’s how MSME loans and business loans differ across major factors

MSME loans are mainly for small and medium enterprises needing flexible terms, while general business loans offer higher funds for long term strategic investments.

MSME Loan vs Business Loan

Choose an MSME Loan if,

- You operate a micro, small, or medium enterprise

- You need relatively running capital requirements

- You want easier access to credit and lower interest rates

- Your focus is on expansion, inventory or operational stability rather than major capital projects

The Indian government supports MSME credit through Government schemes making debt financing for businesses more accessible and reduced risk for lenders.

Choose a Business Loan if,

- Your business requires large scale capital

- You need funds for business expansion financing or major infrastructure projects

- You can provide collateral or have a strong credit history

Business loans can be particularly useful for enterprises planning acquisitions, long term investments or scaling operations across multiple locations.

Why Working Capital Loans Essential

A working capital loan is ideal when your focus is short term liquidity. Businesses often face timing mismatches between receivables and payables, seasonal fluctuations or unexpected cash crunches and working capital financing solutions helps fill these gaps.

Uses of a Working Capital Loan

- Inventory financing solutions

- Paying salaries and wages

- Managing day to day operations

- Bridging gaps in cash flow management for businesses

This kind of loan is tailored for working capital management, helping businesses stay flexible, especially during high demand or slow payment periods.

Major Benefits of Each Loan Type

MSME Loan Benefits

- Lower interest rates thanks to government subsidy schemes

- Easier documentation and eligibility criteria

- Collateral free options available

- Encourages MSME funding for growth and stability

- Builds credit history for future borrowing

MSMEs often struggle to secure formal credit, only about 14% of MSMEs in India have access to formal financial credit, making these loans vital for sector growth.

Business Loan Benefits

- Larger funding amounts for strategic growth

- Can support long term projects or technology investments

- Multiple repayment options and flexible tenures

Business loans can deliver deeper financial muscle to companies with established credit and revenue, which is essential for scaling large operations.

Working Capital Loan Benefits

- Improves liquidity and cash flow management for businesses

- Handles seasonal business swings with ease

- Helps maintain supplier relationships through timely payments

- Enables smoother payroll and operational cycles

Working capital loans ensure your business stays operational even during tough cash flow cycles.

Current Lending Landscape & Statistics

Understanding the broader lending ecosystem helps frame the importance of these loans in real business scenarios,

MSME Credit Growth

- Totally MSME’s business credit exposure in India recently hit approximately ₹46 lakh crore, with working capital loans forming about 57% of outstanding credit, showing how crucial working capital financing solutions are to business sustainability.

Loan Demand & Credit Gap

- Despite strong credit demand, India’s MSME sector faces a large financing gap estimated around ₹28 lakh crore indicating huge unfulfilled need for MSME funding and credit solutions.

Contribution to Economy

- MSMEs contribute nearly 30% to India’s GDP and play a vital role in employment and exports, underscoring why MSME loan benefits have wide economic impact.

These numbers demonstrate how financing options like MSME business loans, business loan benefits, and working capital loan benefits don’t just help individual businesses, they support whole sectors and economic growth.

What You Should Know about Long Term vs Short Term Business Loans

When comparing loan types, it’s vital to consider long term vs short term business loans,

- Short Term Loans like working capital loans typically have tenures under 12-18 months and help with immediate fund needs.

2. Long Term Loans such as business loans (including large MSME loans) may have multi year repayment schedules, often used for expansion and asset purchases.

Your choice should depend on your cash flow cycle, projected revenue, and funding goals.

Which Loan Is Best for Your Business?

Here’s a quick decision map,

- IF you need operational liquidity or to handle short cycles?

Choose a Working Capital Loan

- You run a small or medium business and want lower costs with government backing?

Go for an MSME Loan - Do you need big capital for expansion or major projects?

A Business Loan is the right option

Conclusion

Finding the right financial product if it’s an MSME loan, business loan or working capital loan can unlock growth, balance and long term success for your enterprise.

From improving working capital management to securing funds for business expansion financing, knowing the strengths and good use cases of each loan type helps you make informed and strategic business decisions.

You’re looking to maximize growth and financial stability while accessing flexible debt options, consider your business needs carefully and choose the product that aligns with your goals.

Explore our multiple Finance Services

FAQ's

1. What are the eligibility criteria for an MSME loan?

To be eligible for an MSME loan, businesses typically must be registered as micro, small, or medium enterprises under MSME/Udyam criteria, have valid GST & PAN, be operational for at least 1-2 years, demonstrate stable revenue and repayment history, and have a decent credit score (often 650+). The applicant’s age usually must be between 21 and 65 years.

2. What is the basic eligibility criteria for a business loan?

Business loan eligibility generally requires,

- Registered business entity (proprietorship, partnership, Pvt. Ltd., LLP)

- Minimum operational history (varies by lender)

- Good credit score (700+ often preferred)

- Financial statements & GST return

Lenders assess business viability, cash flow, and repayment capacity.

3. What are the eligibility requirements for a working capital loan?

Working capital loans usually require,

- Business registration in India

- At least 2 years of operation or financial history

- Good credit history (700+) and clear tax returns

- Healthy financial performance as per balance sheets

Some lenders may ask for collateral, while others offer unsecured options.

4. What is the interest rate on MSME loans in India?

MSME loan interest rates vary widely depending on lender and scheme:

- Public sector banks: ~8.5% – 11.5% p.a.

- Private banks: ~9.5% – 14% p.a.

- NBFCs: ~12% – 18% p.a.

Government linked loans can be lower with subsidies.

5. What are typical business loan interest rates?

Business loan interest rates fluctuate based on lender risk assessment, borrower profile, and secured vs unsecured status. Typical unsecured business loans can range from 15% to 28% p.a. in some lenders’ products.

6. How do interest rates for working capital loans compare?

Working capital loans generally have competitive interest rates that reflect short term financing risk and borrower credit score. Some schemes offer subsidized rates, especially under government guarantee programs sometimes with interest subvention on working capital.

7. What is the usual MSME loan repayment tenure?

MSME loans can offer flexible tenures, commonly from 1 year up to 15 years, depending on loan product and purpose (expansion, equipment purchase, etc.).

8. How long is the repayment period for business loans?

Business loans often have tenures ranging from 6 months to 5 years for short term needs, and up to 10+ years for long term investments, depending on the lender and loan type.

9. What is the typical working capital loan tenure?

Working capital loans are usually short term to medium term, often spanning 1 to 3 years, with renewable credit facilities like overdraft or cash credit lines that reflect the cyclical nature of business cash flow.

10. Are collateral free MSME loans available?

Yes, under CGTMSE (Credit Guarantee Fund Trust for Micro & Small Enterprises), MSMEs can access collateral free loans up to ₹2 crore, with the trust guaranteeing 75%-85% of the loan value. This has helped facilitate over ₹8 lakh crore in loans nationwide.

11. What is an unsecured business loan?

An unsecured business loan does not require collateral. These are popular for small businesses but typically come with higher interest rates due to increased risk for lenders. Eligibility still depends on credit history and business cash flow.

12. What are the main types of business loans?

Common business loan types include,

- Term loans (short, medium, long)

- Working capital loans

- Overdrafts & cash credit

- Equipment financing

- Invoice discounting & letter of credit

- Government guaranteed loans

13. What small business loan schemes are offered by the Government of India?

Key schemes include,

- CGTMSE – Collateral free loans up to ₹2 crore

- Stand Up India – Loans ₹10 lakh to ₹1 crore for women & SC/ST entrepreneurs

- PMEGP – Subsidized capital for new ventures

14. What is the difference between SME and MSME loans?

Both serve small enterprises, but MSME loans specifically target micro, small, and medium enterprises under government classification and often include dedicated government schemes, subsidies, or guarantees that may not be available under general SME loans.

15. Can working capital loans be used for business expansion?

Working capital loans are not ideal for long term expansion. They are meant for short term liquidity and recurring operational expenses.